Background

In Mariotto v. Rowntree Estate, 2026 BCCA 215, the British Columbia Court of Appeal considered the proper application of negative contingency deductions where a plaintiff has significant pre-existing health conditions. The decision provides important guidance on the evidentiary foundation required to justify substantial reductions in damages based on the possibility that a plaintiff would have suffered similar losses irrespective of the defendant’s negligence or tortious conduct.

The Plaintiff, Kristina Mariotto, was injured in a low-speed rear-end motor vehicle collision in July 2018. Liability was admitted, leaving only the assessment of damages for trial. Although the collision caused minimal vehicle damage and minor physical injuries, the plaintiff alleged that it triggered severe and lasting cognitive and psychological impairments that significantly affected her employment, daily functioning, and quality of life.

Prior to the accident, Ms. Mariotto had a documented medical history that included Addison’s disease, hypothyroidism, asthma, migraines, and other health conditions. Despite these issues, the evidence demonstrated that she maintained steady employment, remained physically active, and functioned independently. Following the accident, however, her mental state deteriorated dramatically. The trial judge accepted that her symptoms were genuine and debilitating but rejected her theory that she had suffered a concussion or mild traumatic brain injury. Instead, the judge concluded that her condition was likely multifactorial and most consistent with a somatic symptom disorder.

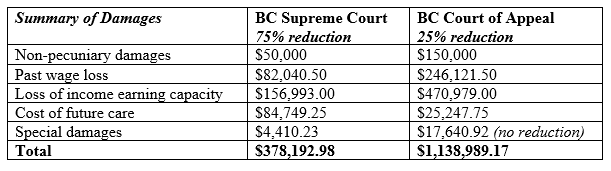

The trial judge found that the accident played some role in the plaintiff’s decline but concluded there was a high likelihood that she would have developed a similar condition following another minor life event because of her psychological vulnerability. On that basis, the trial judge applied a 75% negative contingency deduction across all heads of damages, reducing the award from approximately $1.6 million to approximately $378,000.

The Plaintiff/Appellant appealed the trial judgment’s assessment of the contingency deduction in its totality and in its general application to all heads of damages.

The Court of Appeal’s Decision

The Court of Appeal allowed the appeal and significantly increased the damages award. The central issue was whether the 75% contingency deduction was supported by the evidence and consistent with the principles governing specific contingencies.

The Court reaffirmed that a defendant bears the burden of proving a “real and substantial possibility” that a plaintiff’s pre-existing condition would have resulted in similar losses regardless of the defendant’s wrongdoing. Once that threshold is met, the court must assess the relative likelihood of the contingency materializing. This framework, established in Dornan v. Silva 2021 BCCA 228, requires an evidentiary basis for both the existence and quantification of the contingency.

While the Court accepted that the plaintiff possessed a psychological vulnerability that could qualify as an “extreme vulnerability” under the contingency analysis, it found that the trial judge’s assessment of a 75% likelihood was unsupported by the evidence. The Court observed that the plaintiff had experienced previous accidents and other life events without developing similar symptoms. There was no evidence demonstrating that an everyday mishap was highly likely to trigger the same debilitating condition. As a result, the 75% deduction was characterized as “untethered to an evidentiary basis.”

The Court concluded that a negative contingency deduction was warranted but fixed it at 25%, reflecting a real but relatively unlikely possibility that the plaintiff would have experienced a similar outcome absent the accident.

The Court also held that the trial judge erred by applying the deduction to special damages. Past expenses that have already been incurred are not subject to future contingency reductions. The Court therefore restored the plaintiff’s special damages in full.

The revised award increased the plaintiff’s total recovery to approximately $1.14 million.

Key Takeaways

The decision reinforces several important principles in personal injury litigation. Remember the two-step framework from Dornan for negative contingency deductions:

• A pre-existing condition may constitute a specific, negative contingency if, on the evidence, there is a real and substantial possibility that the pre-existing condition would detrimentally affect the Plaintiff in the future, regardless of the Defendant’s tortious conduct; and

• If the real and substantial possibility is established, the court must then assess the relative likelihood of that possibility materializing.

1. Consider the distinction between establishing the existence of a contingency and quantifying its likelihood. A defendant may successfully demonstrate a real and substantial possibility of future impairment, yet still fail to justify a large percentage deduction. The percentage selected must be supported by the evidentiary record.

2. Special damages should not be reduced by future contingencies because they represent actual expenses already incurred. Parties must carefully consider whether a contingency logically applies to a particular head of damage before applying a deduction.

3. The decision also serves as a reminder of the importance of expert evidence. The trial judge noted the absence of testimony from key treating physicians, including an endocrinologist, despite the central role played by the plaintiff’s pre-existing Addison’s disease. Where pre-existing medical conditions are relied upon to justify substantial reductions in damages, comprehensive expert evidence will often be critical.

/Passle/593009bf3d94760454b5e183/SearchServiceImages/2025-07-04-19-54-57-855-686831918714336e9f5574a9.jpg)

/Passle/593009bf3d94760454b5e183/SearchServiceImages/2026-06-19-20-36-53-147-6a35a865173c792455c3ab9e.jpg)

/Passle/593009bf3d94760454b5e183/SearchServiceImages/2026-06-19-20-42-30-544-6a35a9b6173c792455c3b08e.jpg)

/Passle/593009bf3d94760454b5e183/SearchServiceImages/2026-06-09-16-45-18-724-6a28431ee22b6af8adca1520.jpg)